What do these recent OCR cuts mean?

August 16, 2024

Here are my 7 reasons OCR cuts won’t ignite house prices:

- Restrictive Bank Lending: Banks remain conservative in their lending practices, as highlighted by the Reserve Bank in their accompanying presentation when questioned about the potential for house price increases.

- Economic Struggles: The economy is struggling, with the Reserve Bank predicting a technical recession for the rest of the year. Rising unemployment, government spending cuts, and job reductions contribute to a very low general sentiment.

- High Stock Levels: Many people who postponed selling their properties over the last three years have now entered the market, resulting in higher supply relative to demand.

- Investor Absence: Investors are largely absent from the market. Baby boomers are net sellers of investment properties, despite the gradual improvement in some fundamental investment return drivers after facing the worst regulatory and market conditions in memory.

- Shift Away from Property Investment: A trend away from property investment is evident among the new generation of workers, especially in Wellington. Investors are often perceived as greedy landlords, making property investment less popular. However, owning a home to live in remains a goal, with people prioritizing lifestyle and social responsibility.

- New Loan-to-Income Ratios: The new loan-to-income ratios limit banks to lending less than six times the borrower’s income. While this won’t have a significant effect with current high-interest rates, it could prevent some marginal lending if interest rates drop considerably.

- Immigration is Slowing: After record net migration last year, it is now rapidly declining, with a peak to trough drop of nearly 50% by June this year.

Understanding Real Estate Cycles

Real estate is highly cyclical, driven primarily by the credit cycle—the cost of credit and access to it. However, many variables are at play. Real estate is an illiquid market that doesn’t change course quickly. The real estate cycle typically follows a roughly 7-to-10-year pattern, driven by several factors:

- Economic and Credit Fundamentals: After a downturn, both economic and credit market fundamentals must improve.

- Underbuilding Periods: During the bottom of the cycle, underbuilding tightens supply.

- Easing Credit Restrictions: An easing of credit restrictions, cheaper capital, and population growth often trigger a gradual upward trend in prices.

- Market Participation: As prices rise, more investors, speculators, and first-home buyers enter the market, driven by a “fear of missing out.”

- Booming Economy: A booming economy, partly fuelled by the wealth effect of rising house prices, cheap credit, and severe “fomo” eventually lead to a frenzy in house buying.

This process unfolds over years, which is why real estate tends to get interesting in the latter half of the economic cycle—not in the middle of a recession!

Historical Perspective

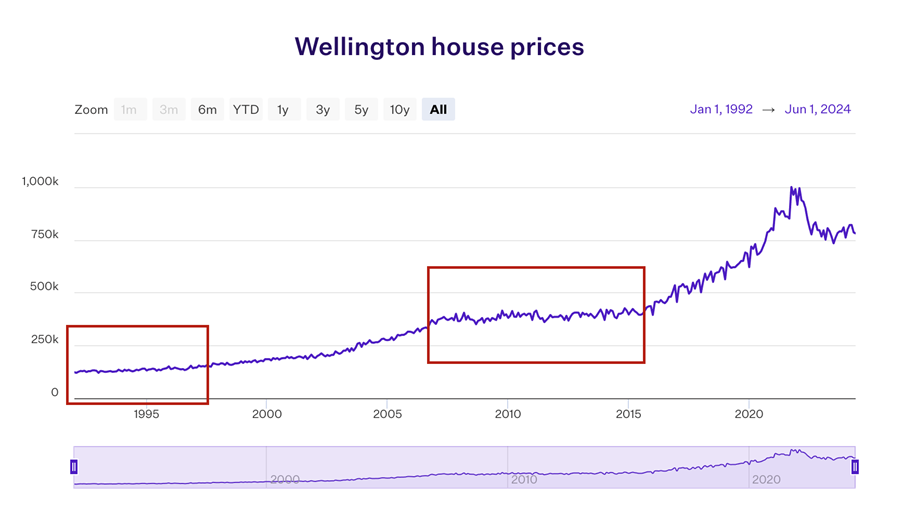

Looking back, we see this cycle play out repeatedly. After the GFC in 2008/09, it took seven years for Wellington prices to start rising again, even as interest rates declined rapidly. History doesn’t repeat itself, but it often rhymes. I’ve highlighted past long stagnant periods in the following graph (credit: Opes Partners).

Moving Forward

In the short term, there will be price volatility driven by changes in supply and demand. The number of houses sold each year is still artificially low, with many buyers and sellers still on the side-lines, but turnover will continue to recover (thankfully for us brokers). However, sustained, inflation-beating capital gains could be several years away, in my opinion.

Looking further ahead, it’s reasonable to hypothesize that long-term gains may not be as pronounced as those over the last 40 years, due to the structural decline in interest rates in that time. As the cost of funding dropped and wages grew, house prices appreciated while households became more indebted through each cycle. It seems a reasonable bet that this cannot repeat, with interest rates reaching the ~0% floor in recent years. It seems logical that interest rates will be more “range-bound” through future cycles. House prices have compounded at > 7% in the last 40 years; it wouldn’t be surprising if the average compound rate of return drops by a percent or two over the next 40 —alongside lower inflation in general. Either way, human nature will ensure house price movements remain as cyclical as ever.

On the positive side, we can see the key fundamentals shifting. Building consents have dropped like a stone. The credit loosening cycle has started. Regulations on investors have eased. Property prices are below long term trends. All these things will setup the next upward leg in time. The purpose of this article is to attempt to answer the implicitly optimistic question I keep getting: will the OCR cuts raise house prices? My answer is: not quickly. Obviously, I do not know what will happen. This is simply my opinion.

Final Thought

Perhaps counterintuitively considering the tone of these comments, I believe it is an amazing time to buy! Just temper your expectations for medium-term growth, focus on cash flow and affordability, and take a long-term view. Had you purchased during the post-GFC stagnation, you would be very pleased with your decision today—even after the recent 26% price decline!