The Wellington Deposit Gap: How Much Deposit Do First-Home Buyers Really Need in 2025?

November 21, 2025

For years, Wellington first-home buyers were told a simple rule: you need a 20% deposit to buy a house. But lending criteria, government schemes and lender flexibility have evolved — meaning some Wellington buyers can now enter the market with as little as 5 %, depending on eligibility and property type.

If you’ve been wondering how much deposit first-home buyers need, the answer in 2025 is: Wellington first-home deposits range from 5% to 20%. Your pathway depends on your income, credit history, property choice, and whether you qualify for Kāinga Ora’s First Home Loan programme. Let’s unpack what’s really happening in Wellington right now.

The 20% Deposit Benchmark: Why It’s No Longer the Only Way

The 20 % rule came from the Reserve Bank’s loan-to-value (LVR) restrictions, designed to manage risk across the housing market. It became real-estate folklore — passed down from parents to kids — even though modern lending and government support have changed the rules.

Today, some first-home buyers in Wellington are purchasing with 5% deposits (via the First Home Loan scheme). Deposits of 7–10% may also be possible where lenders permit and risk criteria are met — though this is less common.

While a 20% deposit still helps reduce loan costs and low-equity fees, it’s no longer a fixed requirement for all buyers.

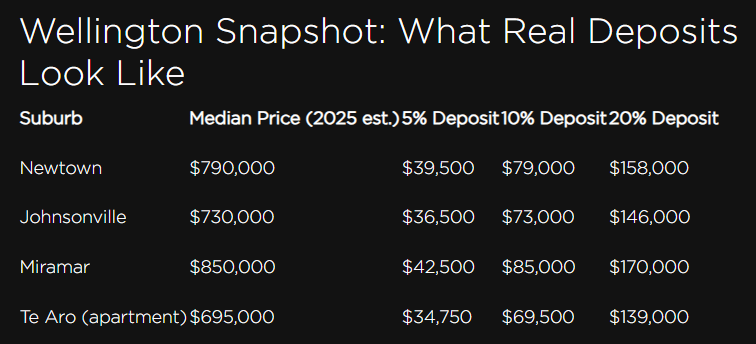

Wellington Snapshot: What Real Deposits Look Like

*Based on REINZ March 2025 data and Lowe & Co sales records (indicative only). The Wellington regional median price in March 2025 was around $800K (REINZ Monthly Report April 2025). In October 2025, Wellington's medium price was $760,000.

With Wellington’s median home price in the ballpark of $800,000 (REINZ, March 2025), smaller deposits can open doors in suburbs once out of reach. The city’s stable employment base and public sector workforce also help lenders remain flexible.

The 5% Deposit Path: Kāinga Ora’s First Home Loan

If you have a stable income but modest savings, this scheme lets you buy with just 5 % down

Eligibility (as at 2025):

- Income caps — $95K (single) | $150K (couple)

- Price cap (Wellington) — up to $800K (existing or new home)

- You must live in the property

- Participating lenders — ANZ, Westpac, SBS Bank and others

- Mortgage insurance premium rising from 0.5 % to ≈ 1.2 % for new applications lodged after 1 July 2025 (subject to official confirmation)

Sources: Kāinga Ora – First Home Loan (2025) | RNZ Budget 2025 Report

Deposit Strategies Beyond Saving

Saving isn’t the only way to build your deposit. First-home buyers are combining multiple tools to close the gap faster.

Using KiwiSaver

After three years of contributions, you can withdraw nearly your entire KiwiSaver balance (keeping $1,000 in the account) to fund your first home. You may also qualify for up to $10,000 in First Home Grants.

To be eligible, you must: - Have been a KiwiSaver member for at least three years (Inland Revenue) - Leave at least $1,000 in your account after withdrawal - Intend to live in the home you’re buying (it must be in New Zealand) - Apply before settlement, as withdrawals usually take up to 10 business days to process (Smith Partners)

You can withdraw your contributions, your employer’s contributions, and investment returns — but not the original government kick-start or funds transferred from an Australian super scheme. (Kāinga Ora)

Gifting, Family Support & Springboards

Gifted deposits are increasingly common — most banks accept them if a signed declaration confirms the funds don’t need repayment. Some parents are also using their home’s equity as security, creating a “family springboard.”

Equity Leverage

If you already own property, you may borrow against your equity to fund another purchase — seek independent mortgage and legal advice first. Source: BNZ – Using Home Equity (2025)

Questions to Ask Lenders (and Builders!)

Before signing, first-home buyers should always ask:

- What low-deposit options do you offer?

- What are your low-equity fees or rate loadings?

- Can I combine KiwiSaver and a First Home Loan?

- What’s your policy on gifted deposits?

- Are there restrictions on apartments or new builds?

Bonus tip: Viewing a new build? Prepare a checklist of questions to ask when viewing a new build house — including build guarantees, completion dates, and title handover.

Smart Moves to Bridge the Deposit Gap Faster

- Set small targets: 5 %, 7 %, 10 %

- Automate savings to a high-interest account

- Use bonuses or tax refunds to top up

- Explore co-ownership with family or friends

- Stay updated — RBNZ reviews LVR rules regularly

What’s Next: 2026 and Beyond

As of November 2025, the Reserve Bank has proposed allowing banks to allocate up to 25 % of new owner-occupier loans to borrowers with less than 20 % deposit, if the proposal is implemented. If credit conditions stay stable, 2026 could bring even more flexible low-deposit products from major lenders.

Final Word: From Saving to Owning

You don’t need to wait years to reach a perfect 20% deposit. In Wellington’s evolving market, the right strategy can help you move from saving to owning much sooner.

Your next steps:

- Check your KiwiSaver eligibility.

- Explore Kāinga Ora’s First Home Loan.

- Compare at least two lender offers.

- Calculate what a 5–10% deposit could buy.

- Talk to a Lowe & Co agent for tailored advice on Wellington’s first-home options.

FAQ: Quick Answers for Wellington First-Home Buyers

Q: How much deposit do first-home buyers need in Wellington?

Anywhere from 5% – 20%, depending on lender and scheme eligibility.

Q: How does KiwiSaver work for first-home buyers?

After three years, you can withdraw your balance (leaving $1,000) and may qualify for up to $10,000 in grants.

Q: Can I use equity from one house to buy another?

Yes — but consult your lender about risks and conditions.

Q: What’s the lowest deposit available in NZ right now?

5% under Kāinga Ora’s First Home Loan.

Q: What should I ask when viewing a new build house?

Ask about warranties, completion timelines, and compliance certificates.

Ready to Make Your Move?

Connect with Wellington’s most awarded real-estate team — Lowe & Co Realty. Our agents work closely with local lenders and buyers to help you navigate deposits, KiwiSaver, and new-build opportunities.

Disclaimer: This article is for general information only and does not constitute financial or legal advice. Lending criteria, income caps and interest rates change frequently and differ by lender. Readers should seek independent advice from a licensed mortgage adviser or lender before making any decisions. Lowe & Co Realty does not provide financial services or brokerage advice under the Financial Markets Conduct Act 2013.