Wellington Real Estate 2025: Have We Hit the Bottom?

December 17, 2025

Making sense of Wellington’s ‘flat but flexing’ market

Wellington real estate has been through a turbulent few years — sharp rises, a significant correction, and a long period of relative stability. While the most dramatic movements ended in late 2022, the market has remained broadly stable since then, with recent data indicating early signs of renewed stabilisation after a softer patch in 2024–2025.

Latest QV data shows Wellington house prices are now up to around 30% below their peak, making it one of the hardest-hit markets in the country.

At the same time, supply has surged and interest rates have eased from their highs, creating a market that is “flat but flexing” rather than in free-fall.

For cautious, data-minded Wellington buyers and sellers, the key questions are:

- Has the correction run its course?

- Is this a safer window to act — or is there more downside to come?

- How should you respond if you’re worried about mistiming your move?

Wellington 2025 Snapshot: Flat but Stabilising

- Values: Around 30% below peak in Wellington, according to QV and recent media reporting.

- Recent trend: A 0.3% lift in Wellington’s average property value in late 2025, ending an eight-month decline and bringing the average to about $943,000.

- Supply vs demand: Housing stock in Wellington is up 4.3% over the five years to 2024, while the population has actually fallen by about 1%.

If you’re feeling cautious: this mix of lower prices, ample supply and modest stabilisation can offer more breathing room and less competition for buyers — but it also means you shouldn’t expect a rapid rebound if you’re a potential seller.

1. What’s Really Driving the Wellington Real Estate Reset?

Why prices fell ~30% — and why that’s only part of the story

From late 2020 into 2021, Wellington house prices surged on the back of record-low interest rates, strong pandemic-era demand and tight supply. Opes Partners

From early 2022 onwards, that picture reversed:

- The Reserve Bank lifted the OCR aggressively, pushing mortgage rates much higher.

- Buyers’ borrowing power fell, and demand cooled.

- A large pipeline of homes consented during the boom continued to be completed even as demand fell, contributing to today’s oversupply. RNZ+1

Cotality’s analysis shows Wellington’s stock growth outpaced population change significantly between 2019–2024, producing a structural, supply-driven shift in the market. Cotality+2Good Returns+2

Rather than a “crisis” of shortage, Wellington now faces the opposite: more homes, fewer people, and a market recalibrating to higher interest rates. This is a structural correction — not a systemic crash.

For cautious buyers and sellers:

This makes planning more reliable. The correction has been steep, but it reflects fundamentals rather than instability.

2. Signs Wellington Is Stabilising — What the Latest Data Shows

Modest value growth returns

OneRoof’s November 2025 House Price Report notes that Wellington’s average property value rose 0.3% to about $943,000, ending an eight-month run of declines that together shaved around 5% off prices.

The report also highlights:

- A lift in buyer enquiry levels, especially in lower price brackets.

- More realistic vendor expectations as sellers accept that peak-era values are gone.

Local agent feedback echoes this: well-presented, realistically priced homes in value-sensitive suburbs (for example, parts of Newtown, Tawa, Island Bay and the Hutt Valley) are seeing better attendance at open homes and more consistent offers.

Supply remains elevated, demand cautious

Cotality and related coverage show Wellington’s housing surplus is now a meaningful headwind to sharp price rebounds: more homes per resident means buyers have more choice and can take their time.

At the same time, ANZ and other forecasters describe the national market as “broadly flat” through 2025, with modest improvement expected in 2026 if rates continue to ease and the economy strengthens.

Why stabilisation matters more than the peak-to-now drop:

For “cautious opportunists”, a flat, more predictable market reduces timing risk. You’re not trying to catch a falling knife — you’re operating in a market that is bumping along a floor.

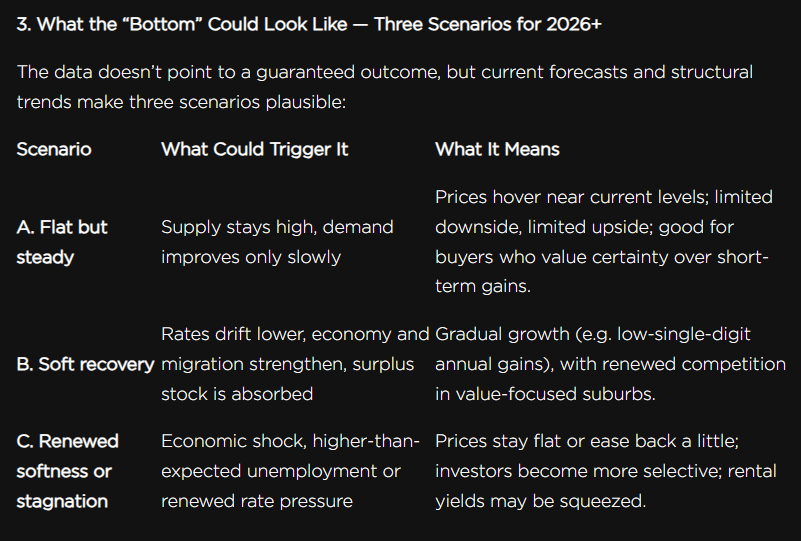

3. What the “Bottom” Could Look Like — Three Scenarios for 2026+

The data doesn’t point to a guaranteed outcome, but current forecasts and structural trends make three scenarios plausible:

Key point:

Most major outlooks suggest modest, not dramatic moves from here. For many Wellington buyers and sellers, strategy will matter more than perfect timing.

4. What This Means for Buyers, Sellers & Investors

First-Home Buyers — The Cautious Opportunists

Why this phase can work in your favour

- Prices are significantly below the peaks, making affordability the best it’s been in several years in many parts of New Zealand.

- Higher stock and slower sales give you more time to do due diligence and negotiate.

- Turnkey or low-maintenance homes in suburbs such as Berhampore, Tawa, Kilbirnie and Brooklyn are still in demand, but competition is more measured than in 2021.

What to watch

- Interest-rate moves and bank servicing rules (these affect what you can borrow).

- Listing volumes and days-to-sell in your target suburbs — these show how much leverage you really have at the negotiation table.

Prudent approach

If you can comfortably service a mortgage with a buffer for future rate changes, a flat market can be a sensible entry point — especially if you’re planning to hold for the long term.

Sellers — Especially Those Who Bought Near the Peak

Reality check from the latest data

- QV and media reporting confirm Wellington values are around 30% below peak, and still easing in some segments.

- OneRoof’s suburb data shows some areas are still below 2020 price levels.

What this means in practice

- Pricing at or near recent comparable sales, rather than 2021 expectations, is essential.

- In a flat market, marketing quality, property presentation and agent reach can be the difference between selling and sitting.

If you don’t have to sell, you may choose to hold and wait for a soft recovery. If you do need to sell, focusing on presentation and correct pricing can still deliver strong outcomes in the context of today’s values.

Investors & Long-Term Holders

Opportunities

- Lower entry prices improve the relationship between rent and mortgage costs compared with the peak.

- A period of sideways prices can be an opportunity to accumulate quality assets if your cashflow allows.

Risks

- A sustained surplus of stock could cap rent growth or increase vacancy periods in some pockets.

- If economic conditions soften more than expected, yields may come under pressure.

A long-term, fundamentals-first approach — focused on quality locations, realistic yields and conservative leverage — is more important than ever.

5. The Key Wellington Metrics That Matter Most

If you’re trying to make a data-informed decision, not all numbers are created equal. Focus on:

- QV House Price Index & Cotality Home Value Index

These show medium-term trends rather than noisy monthly moves. - Dwelling stock vs population growth

In Wellington, stock has grown faster than population, loosening the supply–demand balance and helping keep a lid on prices. - Listing volumes, days to sell and clearance rates

These are the real-time heartbeat of buyer demand and seller motivation. - Suburb-level values and sales data

OneRoof’s reports show large differences even within Wellington; some suburbs are only slightly off peak, others are well down. - Interest-rate and macro outlook

ANZ and other major banks currently expect broadly flat prices through 2025, with a gradual improvement in 2026 if the OCR continues to fall and growth improves.

6. Practical Checklist If You’re Unsure What to Do

- Clarify your goal: first home, upgrading, downsizing, investing, or freeing up capital.

- Stress-test your numbers: model your cashflow at interest rates 1–1.5% higher than today. Reserve Bank of New Zealand

- Zoom in: look at suburb-specific values, days-to-sell and yields, not just Wellington citywide averages.

- Seek local, independent advice: experienced Wellington agents and advisers can help interpret the data for your specific property type and suburb.

- Think in years, not months: most credible forecasts point to a period of moderate returns, not another boom-and-bust cycle.

Conclusion — A Sensible Window for Long-Term, Data-Led Decisions

As of late 2025, Wellington real estate prices sit roughly 30% below their peak, but the most recent numbers show early stabilisation rather than continued sharp falls.

For cautious, evidence-driven buyers and sellers, this phase may represent one of the safer windows in recent years to act — provided your decisions are guided by:

- Realistic expectations about price levels

- Careful attention to suburb-level data

- A long-term ownership or reinvestment plan

If you’d like to move from “big-picture headlines” to suburb-specific clarity on your situation:

- Get a suburb-specific breakdown of current values and days-to-sell

- Book a no-pressure chat with a local Wellington expert

- See what similar homes to yours are currently selling for

These steps can help turn a noisy, uncertain market into a clear, confident decision — grounded in current, verified data, not guesswork.