Remortgage or Sell? How to Decide When You’re Ready for a Change of Scene

December 8, 2025

Thinking about a lifestyle change but unsure whether to remortgage to buy a second home or sell your current property altogether? For many Wellington homeowners, the decision comes down to equity, lifestyle goals, and financial comfort. This guide helps you weigh both paths so you can move forward with confidence.

Why Your Wellington Home Matters — and Why You Might Be Ready for Change

Your home is more than an address — it’s your base in one of New Zealand’s most vibrant cities. Yet as lifestyles evolve, so do priorities.Perhaps you’re dreaming of coastal mornings on the Kāpiti Coast or a sustainable retreat closer to nature.

The “Equity-Rich Explorer” Mindset

Over recent years (since around 2015), many Wellington homeowners have seen strong capital gains — though growth has softened (values have suffered) in recent years. According to REINZ data (October 2025), the Wellington region median was around $760,000, down roughly 4 – 5 % year-on-year.

Lowe & Co’s insights, Wellington’s metro average sat around $840,000 for the same period, consistent with Squirrel’s July 2025 Market Update.

These “equity-rich explorers” are now considering how to use their home’s value for lifestyle change — whether that means downsizing, purchasing a holiday home, or funding a more sustainable way of living.

Lifestyle Signals That It’s Time for Something New

Common triggers we see among Wellington homeowners:

- Empty-nest stage and a desire for simpler living

- Remote work flexibility enabling relocation

- Interest in eco-friendly or energy-efficient homes

- Desire to unlock equity for travel, investment, or family support

These changes reflect a broader movement toward balance — financial security paired with lifestyle freedom.

Market Snapshot: Houses for Sale in Wellington City

Current houses for sale in Wellington City include a mix of modern turnkey homes and charming villas — appealing to both sellers seeking strong returns and buyers upgrading within the capital. The median sale price sits near NZ$760,000, down around 4.4% year‑on‑year, offering opportunities for well‑prepared buyers. (Squirrel Property Market Update, July 2025)

Option 1: Remortgage to Buy a Second Home

Remortgaging lets you borrow against the equity you’ve built in your current property to fund another home — either for lifestyle, investment, or family support.

Remortgage to Buy a Second Home — How It Works and When It Makes Sense

Remortgaging can help you unlock built‑up home equity to finance another property — whether for lifestyle, investment, or family support.

What Does “Remortgaging” Mean in NZ?

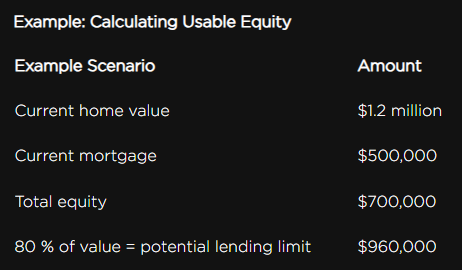

In New Zealand, remortgaging means borrowing against the equity you’ve built in your existing property. Many lenders may issue loans up to 80 % of your home’s current value (i.e., an 80 % LVR), subject to income, expenses, serviceability, property type and other criteria. As of late 2025, fixed mortgage rates were generally in the mid‑4 % range for 4‑ to 5‑year terms, though actual rates vary by lender and borrower profile. (Opes Partners Interest Rate Report, Oct 2025).

How Remortgaging Works in NZ

“Remortgaging” in New Zealand means applying for a new or additional loan using your existing home as security. Most lenders will consider lending up to 80 % of your home’s current value (an 80 % LVR) for owner-occupied properties — provided you meet income, expense, and serviceability criteria. (Kiwibank 2025)

Approx. “usable equity” available to borrow

~$460,000 (before fees and conditions)

Check figures using the MoneyHub NZ equity calculator or your lender’s online tools (e.g. ANZ or Kiwibank).

You can check your figures with NZ’s major lenders — ANZ, Kiwibank, or MoneyHub’s calculator.

When a Remortgage Makes Sense

Remortgaging can be effective if you:

- Have strong income and serviceability capacity

- Want to retain your Wellington base while buying a coastal or greener retreat

- Plan to generate rental income from one property

- Wish to support family through inter-generational property ownership

As of October 2025, fixed mortgage rates for 4- to 5-year terms were generally in the mid-4 % range (Opes Partners Interest Rate Report, Oct 2025).

Risks and Realities

Owning two homes means twice the commitment. Consider:

- Exposure to interest-rate changes

- Maintenance and rental management costs

- Loan-to-value restrictions and tax implications

Important: Always seek advice from a licensed mortgage broker, financial adviser and tax specialist before restructuring loans or buying an additional property.

Option 2: Sell First — The Case for a Clean Slate

Selling before buying gives simplicity and certainty. It’s often best if you’re looking for liquidity, freedom from maintenance, or clarity about your next step.

Advantages of Selling Before Buying

- Simplifies your financial position

- Gives you a clear budget for your next purchase

- Avoids bridging loans and double mortgage stress

- Improves negotiation power as a cash buyer

When Selling Is the Right Choice

Selling may be best if:

- You’re seeking a fresh start or less maintenance

- Your current property has low rental potential

- You need funds for retirement or other investments

Emotional Benefits

Letting go can create space for new beginnings. Many Wellington homeowners find peace in starting over — often aligning the move with sustainability goals and investing in eco-friendly homes in NZ for their next chapter.

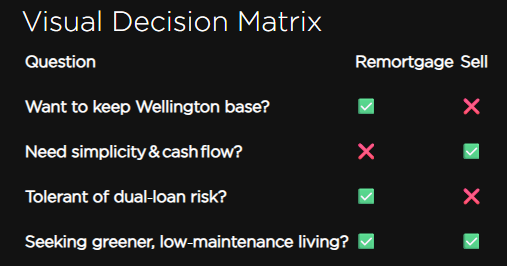

Decision Framework — How to Choose Between Remortgaging and Selling

Use this framework to clarify your best move:

Financial Checklist

✅ How much usable equity do you have?

✅ Can you comfortably service two mortgages?

✅ Have you planned for interest rate fluctuations?

✅ Are there Bright‑Line test or tax implications? (See IRD guidance ➜)

Lifestyle Checklist

✅ Do you need to stay connected to Wellington for work or family?

✅ Are you seeking simplicity or adventure?

✅ Does sustainability feature in your next home goals (e.g., sustainable properties)?

Note: These ticks are illustrative only. Your best path depends on personal circumstances and lender criteria.

How Lowe & Co Supports You Through the Transition

Navigating property change is smoother with the right support team.

Partnering with a Real Estate Buyer's Agent

A real estate buyer's agent helps you identify, assess, and secure your next home — often before it hits the market. Lowe & Co’s agents combine deep local insight with a team‑based model, ensuring you access Wellington’s best opportunities.

Collaboration with Mortgage & Financial Experts

Lowe & Co partners with trusted mortgage brokers and financial specialists who can structure your remortgage safely and strategically. Joint sessions can help you align “property strategy + financial clarity.”

Seamless Transition Support

From appraisals to new‑home searches, Lowe & Co’s agents ensure a seamless experience.

Call to action: Book your free Property Transition Strategy Session to explore your next move with confidence.

FAQs

Can I remortgage my Wellington home to buy another property in NZ?

Yes — if you have sufficient equity and income to meet lender criteria.

What are the risks of owning two homes?

Higher mortgage commitments, rate fluctuations, and maintenance costs. Always budget for contingencies and seek professional advice.

How do lenders calculate usable equity?

Typically, up to 80 % of your home’s value minus your current mortgage. Use ANZ, Kiwibank, or MoneyHub calculators for an estimate.

Is buying a sustainable property more expensive?

Upfront build costs can be higher, but long-term maintenance and energy costs are often lower, and resale appeal is strong.

Final Thoughts — Clarity, Confidence, and Moving Forward

Whether you remortgage to buy your next home or sell and start fresh, the key is understanding your numbers and your “why.” Remortgaging offers flexibility and asset growth; selling delivers simplicity and liquidity. Your best choice depends on your serviceability, risk tolerance, and future vision. You don’t have to decide alone — Lowe & Co’s agents and partner advisers can help you weigh both options clearly and confidently.

Disclaimer: This article is for general information only and does not constitute financial, tax, or legal advice. Lending criteria, interest rates and property values change frequently and vary by lender and individual circumstances. Readers should seek independent advice from a licensed mortgage adviser, tax specialist or lawyer before making any decisions. Lowe & Co Realty does not provide financial services or brokerage advice under the Financial Markets Conduct Act 2013.

Key Verified Sources

- REINZ Monthly Property Report (June 2025)

- Squirrel Property Market Update (July 2025)

- Opes Partners Interest Rate Report (Oct 2025)

- RBNZ LVR Rules Summary (May 2025)

- Kiwibank Next Home Guide (2025)

- IRD Bright-Line Rule Guidance (2025)